경제 / 금융시장 효과

경제 / 금융시장 효과전염 효과

Contagion Effect

한 나라의 위기는 투자자, 대출자, 시장이 다른 나라들을 연결된 위험으로 볼 때 다른 곳으로 퍼질 수 있다. 다만 진정한 전염은 단순한 상호의존성이나 공통된 경제적 취약성과 구분해 보아야 한다.

인기도

유용성

별칭

금융 전염 / 위기 전염 / 통화 전염 / 파급 효과 / 도미노 효과

분야

국제금융 / 거시경제학 / 통화위기 / 은행위기 / 금융시장 / 리스크 관리

정의

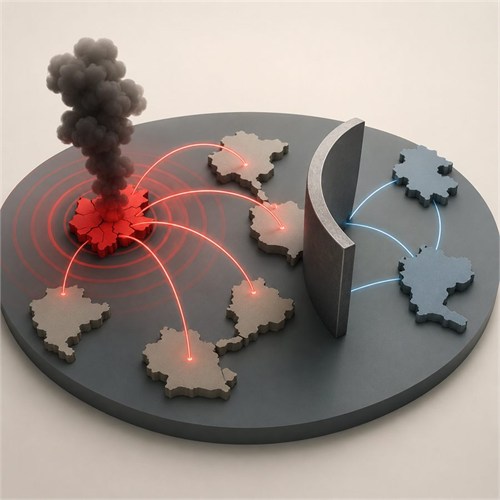

- 전염 효과는 한 나라, 시장, 기관의 금융·경제 위기가 다른 나라나 시장으로 퍼지는 현상을 말하며, 특히 수용 측 국가나 시장이 자국의 기초여건만으로 예상되는 수준을 넘어 영향을 받을 때를 가리킨다. 통화위기 연구에서는 다른 곳에서 위기가 발생했다는 이유로 한 통화에 대한 투기적 공격 가능성이 커지는 현상으로 설명되기도 한다.

핵심 아이디어

- 위기는 투자자 공포, 자본 유출, 무역 연결, 은행 익스포저, 부채 연결, 공통 채권자를 통해 관련 경제나 시장을 ‘감염’시킬 수 있다.

- 시장 연결성이 높고, 신뢰가 약하며, 투자자들이 여러 국가나 자산을 같은 위험군으로 묶어 볼수록 효과는 더 강해진다.

- 오래된 시장 격언이 여전히 들어맞는다. 신뢰가 방을 나갈 때는 좀처럼 조용히 문을 닫고 나가지 않는다.

작동 방식

- 한 나라에서 통화 평가절하, 부채 불이행, 은행 실패, 시장 붕괴 같은 충격이 발생한다.

- 투자자들은 비슷한 나라, 시장, 자산을 재평가하고 자금을 빠르게 회수할 수 있다.

- 통화 매도, 자산 가격 하락, 신용 경색, 유동성 압박이 다른 경제로 퍼진다.

- 이러한 확산은 무역과 은행 대출 같은 실물 연결을 통해서도, 공황, 군집 행동, 포트폴리오 재조정 같은 심리적·금융적 연결을 통해서도 일어날 수 있다.

- 연구자들은 진정한 전염과 정상적 상호의존성을 구분한다. 전염은 충격 이후 교차시장 연결이 유의하게 강화되는 것을 뜻하고, 상호의존성은 위기 전부터 시장들이 이미 강하게 연결되어 있던 상태를 뜻한다.

활용 예시

- A국의 통화가 붕괴한 뒤 투자자들이 B국과 C국도 비슷한 부채, 은행, 수출 위험을 가졌다고 보고 그 통화까지 매도한다면, 이는 가능한 전염 효과다.

- 예문: “1997년 태국 바트화 위기는 아시아 여러 지역으로 금융 전염을 일으켰다.”

대표 사례

- 사례: 1997년 아시아 금융위기. 이 위기는 1997년 7월 태국에서 시작되어 동아시아 전역으로 퍼졌고, 다른 지역에도 파급 효과를 남겼다.

- 이 규칙에 부합하는 이유: 태국의 통화위기 뒤에 다른 아시아 국가의 통화, 자산시장, 은행, 경제에도 압력이 번졌고, 이는 지역적 금융 충격이 투자자 행동, 금융 연결, 신뢰 효과를 통해 어떻게 확산될 수 있는지 보여 준다.

적용 사례 / 해당 상황

- 국가 간으로 번지는 통화위기

- 한 은행이나 지역에서 다른 곳으로 퍼지는 은행 공황

- 글로벌 시장으로 확산되는 주식시장 붕괴

- 유사한 재정 또는 대외 취약성을 가진 국가들에 영향을 미치는 국채 위기

- 신흥국 집단에서 자본 유출을 낳는 투자자 공황

- 국경 간 금융안정을 평가하는 리스크 모형

적용하면 안 되는 경우 / 흔한 오용

- 시장이 함께 움직인다고 해서 모두 전염이라고 해석해서는 안 된다. 정상적 상호의존성은 전염과 다르다.

- 두 시장이 동시에 하락했다는 이유만으로 전염을 단정해서는 안 된다. 동일한 글로벌 충격에 함께 반응했을 수도 있다.

- 두 번째 국가의 위기가 주로 자국의 기초여건으로 설명되는 경우에는 전염이라는 용어를 쓰면 안 된다.

- 맥락이 명확히 비경제적이지 않은 한, 금융 전염을 생물학적 전염, 사회적 전염, 감정 전염과 혼동해서는 안 된다.

- “도미노 효과”는 비공식적 설명으로는 쓸 수 있지만, 그 패턴을 묘사할 뿐 원인을 입증해 주지는 않는다.

기원 / 유래

- 제안자: 금융에서의 일반적 “전염 효과” 개념에 대해 명확히 인정되는 단일 제안자는 없다.

- 제안 시기: 알려져 있지 않다. 이 아이디어는 1990년대 국제금융 연구, 특히 투기적 공격과 통화위기 연구에서 두드러지게 부상했다. Eichengreen, Rose, Wyplosz는 1996년에 “contagious currency crises”에 관한 영향력 있는 연구를 발표했다.

- 기원 국가 / 맥락: 국제금융과 거시경제 위기 연구, 특히 통화위기, 신흥시장, 국경 간 금융 불안정성 연구 맥락.

짧은 실천 포인트

- 한 나라의 위기는 투자자, 대출자, 시장이 다른 나라들을 연결된 위험으로 볼 때 다른 곳으로 퍼질 수 있다. 다만 진정한 전염은 단순한 상호의존성이나 공통된 경제적 취약성과 구분해 보아야 한다.